St. Louis Fed: The U.S. Treasury Department is borrowing heavily and the Fed may need to suspend QT to maintain the stability of the banking system

With the U.S. Treasury borrowing heavily in the bill market, the St. Louis Fed noted that to ensure the stability of the banking system, the Fed may need to pause its efforts to reduce its balance sheet.

The U.S. Treasury has sold about $1 trillion in short-term notes since the government suspended the debt ceiling in June. The cash to buy these Treasuries comes from at least two sources: bank accounts or money market funds.

Money market funds have been reluctant to buy these notes recently because they tend to earn more by temporarily holding their funds in the overnight reverse repurchase facility (ON RRP) used by the Federal Reserve.

If too much money comes out of the banking system, lenders may find their reserves are insufficient to meet regulatory requirements, according to a research note this week by St. Louis Fed economists Amalia Estenssoro and Kevin Kliesen. This may force the central bank to suspend its quantitative tightening program (QT).

The risk exists that as quantitative easing continues, ON RRP balances remain sizable and bank reserves account for the majority of the Fed's liability contraction, bank regulatory constraints may come into effect earlier than expected, the two economists wrote.

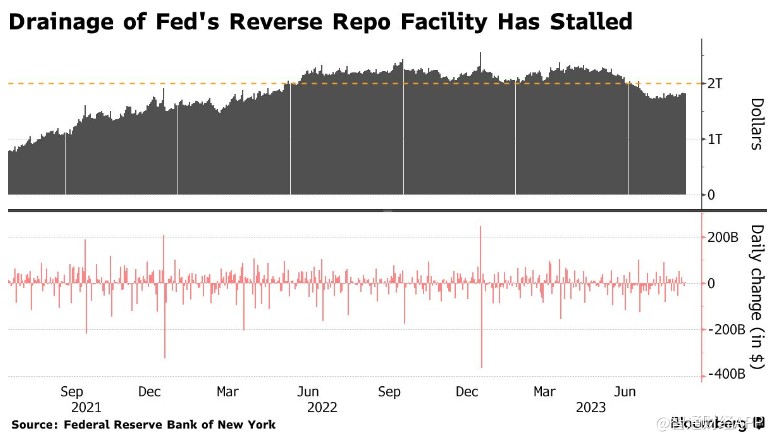

This risk is not purely theoretical, and the decline in the Fed’s ON RRP mechanism appears to have stalled. The scarcity of bank reserves has caused problems in the past, most notably in September 2019, when the Treasury increased borrowing and the Fed stopped buying more Treasuries for its balance sheet.

At that time, overnight funding rates for U.S. Treasury bonds, which Wall Street banks widely relied on, soared, and the Fed eventually intervened to add more reserves to the system by repurchasing those securities.

On the other hand, if funds flow out of ON RRP, the impact on the financial system may be controllable. This seemed to be the direction the financial system was heading nearly three months ago. Demand for ON RRP fell as low as $1.717 trillion on July 18 after the government suspended the debt ceiling. But since then, ON RRP has stabilized at close to $1.8 trillion.

Wall Street strategists estimate that the Treasury Department will need to issue another $600 billion in Treasury bills before the end of this year. But according to economists, this may not completely deplete ON RRP in the second half.

Economists at the St. Louis Fed said that to prevent money market rates from soaring during quantitative tightening about five years ago, bank reserves needed to be equal to about 7% of nominal gross domestic product. At current GDP, this equates to approximately $1.9 trillion in reserves.

But they think a higher level might make more sense. In the Federal Reserve's latest survey of senior financial officials, about 78% of responding bank representatives reported that their institutions preferred to hold additional reserves above their minimum comfort levels.

Estenssoro and Kliesen wrote, "As financial markets continue to evolve, desired liquidity may be closer to 10% to 12% of nominal GDP ($2.7 trillion to $3.3 trillion), and current reserve balances are close to the upper limit of this estimate."